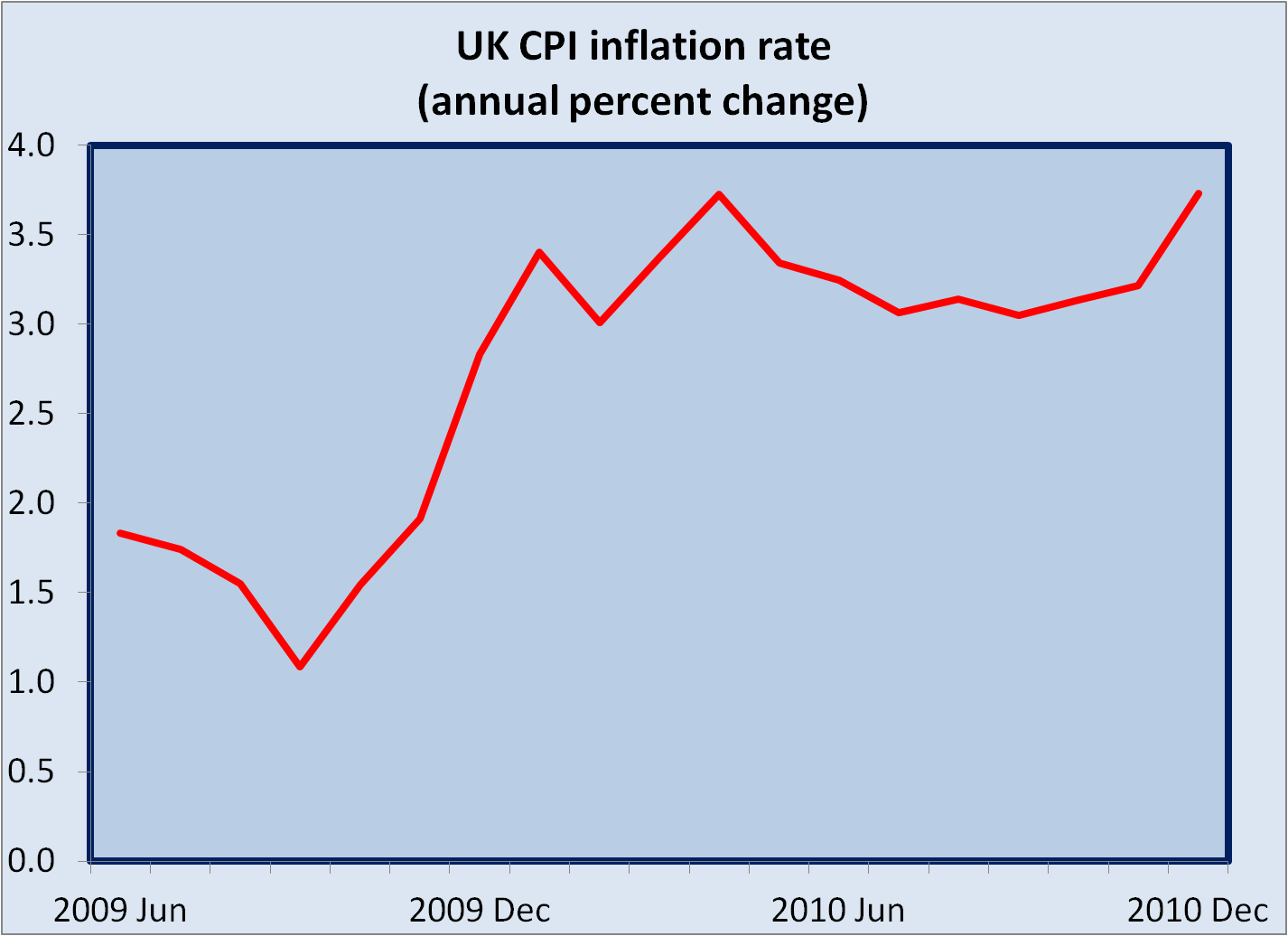

December’s inflation number wasn’t just bad, it was horrific. In just one month the headline CPI rate went up from 3.3 to 3.7 percent. The retail prices index now stands at 4.8 per cent.

To give the December number some context, the CPI rose by one full percent in just one month. This was a record increase. Between 1996 and 2008, the 1-month change between November and December has varied between a fall of 0.4 per cent and an increase of 0.6 per cent. So, the latest number was off the scale. Moreover, this number does not include any of the recent VAT increase. That will hit the index next month.

Notwithstanding the unprecedented nature of the December number, the further deteroriation in inflation should not come as a surprise to anyone. Over the last three years, the Bank of England cut interest rates to near zero, and then followed up by printing billions of pounds. This increase in the money supply has pushed sterling down against all major currencies.

Over in Whitehall the government is running a double digit fiscal deficit, while public sector indebtedness has exploded. It has vacillated over indirect taxation, first cutting the VAT rate and then increasing it twice. Furthermore, these measures were undertaken when oil prices have doubled, and food price inflation is surging. If ever there was a recipe for inflation then this is it.

The standard line to justify this chaotic catalog of policy initiatives is that the financial system has suffered a terrible blow and that these interventions were needed to prevent a 1930s style depression. While it is true that lending activity has slowed, the decline is very much in line with previous post-war UK recessions. Unfortunately, policy makers were far too prone to hyperbole when describing the reasons for their hysterical attempts to keep growth buoyant.

The near-term prospects for inflation are awfully bleak. Without a spectacular change in monetary policy, inflation is going in only one direction. Growth is now picking up, price expectations are rising, and all we need to put us into double-digit inflation territory is a further oil price shock, a renewed surge in food prices, and a marginal acceleration of wage growth.

The monetary policy committee is now cornered. There are no excuses left. There are no more stories to tell about the output gap and how higher unemployment will eventually bring inflation down in the medium term. Without a policy response inflation will quickly slip into double-digit rates in a comparatively short period of time.

There is an understandable concern about how higher interest rates might impact growth. At this stage, a darker scenario is lurking in the corner - capital flight. If investors start to believe that UK inflation will go higher, then either long-term rates rise accordingly, or investors go elsewhere.

This dilemma is likely to manifest itself first in the government bond market. If long rates start to rise, then debt servicing costs will increase as well. Rising long term government bond rates was the trigger that pushed Greece and Ireland over the edge into a full-scale fiscal crisis.

There is one glimmer of hope. The coalition has announced a fiscal consolidation plan that appears to be credible. This has bought the UK economy some time. However, the clock is ticking and that credibility could evaporate as long term interest rates start to rise, putting pressure on a vulnerable deficit position.

The options facing the monetary policy committee are difficult. However, the dangers inherent in a passive approach are exceedingly unpleasant. Whether the MPC likes it or not, the time for a rate hike has come.

No comments:

Post a Comment